Table Of Content

What Is A No Penalty CD?

A no-penalty CD is similar to a traditional one in that it will earn money while it is deposited in the CD. However, there are a few key differences that separate a no-penalty CD and a traditional CD.

- No Penalty Early Withdrawal – one of the main features of this type of CD is that you will not have a penalty if you pull your money out before the contract ends.

- Lower Interest Rates – With the flexibility of no-penalty CDs, the interest rates are lower when compared to traditional CDs. Because of this, your money will not grow as much if it is on a traditional CD.

What Is The Penalty You'll Pay For 12 Months CD?

Every bank or financial institution sets a different penalty. Here are the penalties you'll pay in top banking insitutions if you choose a 12-month CD and withdraw your money before the CD is mature:

Bank/Institution | Early Withdrawal Penalty |

|---|---|

Capital One | 3 months interest |

Citi | 90 days interest |

American Express | 270 days interest

|

Discover | 6 months interest

|

Marcus | 180 days interest

|

Chase | 180 days of interest

|

Wells Fargo | 6 months interest |

We can see Citibank and Capital One charges the lowest penalty. In contrast, American Express charges 270 days of interest, which means if you withdraw your money in the first nine months our of 12 months, you won't earn any interest at all.

How Much Can You Save With No Penalty CD?

If you are looking for an idea about how much you could save if you put your money into a no penalty CD and withdraw early compared to a traditional CD, here are a few different examples.

Considering your deposit of $100,000 and the APR is 4%, here's how much you'll save if yo choose a no penalty CD in each of the following financial institutions if the interest is compounded daily:

Bank/Institution | Early Withdrawal Penalty | How Much You Save? |

|---|---|---|

Capital One | 3 months interest | $991

|

Citi | 90 days interest | $991

|

American Express | 270 days interest

| $3,003

|

Discover | 6 months interest

| $1,992

|

Marcus | 180 days interest

| $1,992

|

Chase | 180 days of interest

| $1,992

|

Wells Fargo | 6 months interest | $1,992

|

However, it's essential to keep in mind that not all of them do offer the option for a penalty CD.

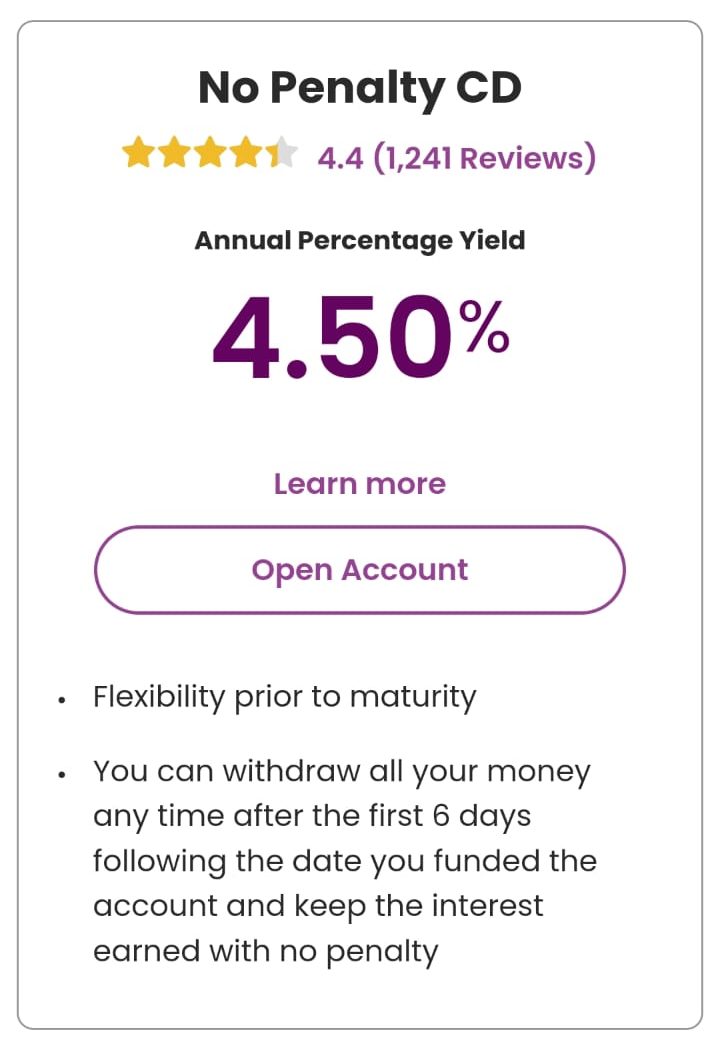

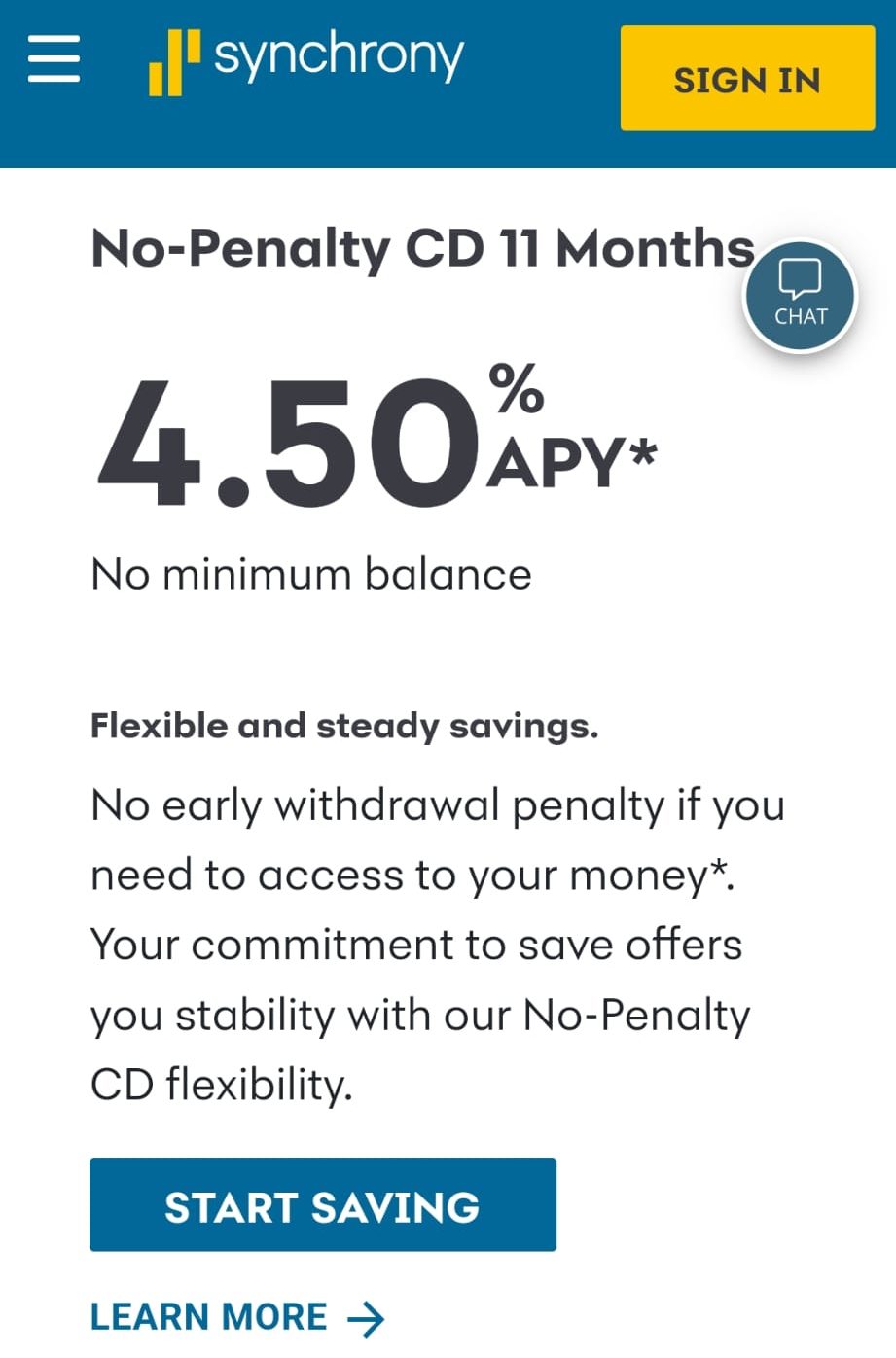

Top Offers From Our Partners

![]()

![]()

![]()

What Are The Terms Of No Penalty CD?

The basic terms of a no penalty CD have an annual percentage yield, the minimum deposit requirement, and the interest compounding frequency.

- The annual percentage yield is the rate that your money will earn over the course of the contract.

- The minimum deposit is how much you have to deposit in order to open the account.

- Finally, interest compounding frequency will either be daily or monthly depending on the contract.

Should I Get a No Penalty CD?

If you are trying to determine whether or not you should invest in a no penalty CD, there are a few positives and negatives that you should consider before putting your money into the CD.

Pros | Cons |

|---|---|

Added Flexibility | Withdrawal Restrictions |

Guaranteed Rate | Deposit Limits |

- Added Flexibility

As opposed to traditional CDs, no penalty CDs offer consumers flexibility with their money since they are able to take their money out without a fee.

This is extremely beneficial if a higher interest rate comes up, allowing you to pull your money quickly and reinvesting it at a higher interest rate. It's also great in times of uncertainty, such as high inflation.

- Guaranteed Rate

No penalty CDs offer a fixed rate that is typically higher than money market accounts and high-yield savings account pay.

- Withdrawal Restrictions

While there is no penalty for early withdrawals, you typically must take out all of the money in the account and close the account instead of making partial withdrawals.

- Deposit Limits

A no penalty CD may only have cash deposited once, when the account is opened. Once the CD is started consumers are unable to make additional deposits into the account.

Where Can You Find No Penalty CD?

Many different financial institutions offer no-penalty CDs. Below is a list of a few different banks and some important information about the no-penalty CD.

Bank/Institution | Term | APY | Minimum Deposit |

|---|---|---|---|

Citi | 12 months | 0.05%

| $500 – $2,500 |

CIT Bank | 11 months | 3.50% | $1,000 |

Marcus | 13 months | 4.70% | $500 |

Ally | 11 months

| 4.00%

| $0

|

- Marcus – Marcus offers a multitude of options for CD rates. As far as no penalty CDs go, they offer a 13-month CD with a 4.70% APY.

- Ally – Ally offers a no-penalty CD option with an APY of 4.00% for their 11-month CD and does not have a minimum deposit. The only downside is that there is only one no penalty CD option.

- CIT Bank – CIT Bank offers no penalty CDs and is rated just a three out of five stars. The APY offered is 3.50% and a minimum deposit of $1,000.

- Citi Bank – With Citi Bank being one of the largest U.S. Banks are able to offer their no penalty CD with a minimum deposit of $500 – $2,500, and an APY of 0.05%.

How To Choose A No-Penalty CD

With many financial institutions offering their own no-penalty CD, some even offering more than one, it is important to keep the following factors in mind when choosing which no penalty CD works best for you.

- Interest Rates – One determining factor for picking a no-penalty CD are the interest rates that are offered. The higher the interest rate being offered, the more rate of return you will receive at the end of your contract.

- Term length – Despite having the ability to pull your funds from the no penalty CD, it is still important to look at how long the contract is. Knowing how long the contract is will give you an idea of how much money you will earn at the end of your contract.

- Minimum deposit – Finally, you must know what the minimum deposit is for the CD, if you do not have that amount you will not be able to open the account.

- Withdrawal Restriction – Typically the financial institution will only allow individuals to withdraw the entire amount of the CD. Because of this, they either have to keep the funds in the account, or close the account by pulling all of the funds out. It is always best to thoroughly read the contract before deciding to put your money into the CD.

How To Open A No-Penalty CD?

If you have ultimately decided the positive features of a no penalty outweigh the negative, actually opening a no penalty CD account is a relatively simple process that is similar across all financial institutions.

- Determine your Price Points – Before reaching out to a financial institution, you must determine how much you are willing to deposit into the account. It is important to set aside a set amount of money that you are willing to not touch for a certain amount of time.

- Pick the Financial Institution – Once you have determined the amount of money you are willing to part with, you are able to pick the financial institution.

- Getting Started Online – Once you have picked the financial institution that you will be investing in, head to their website, select the tab that is labeled “Investments” or “Certificate of Deposits”, and select no-penalty CDs. Once selected, you are able to go on to the next step of getting started.

- Account Type – CD types are varied and include traditional, IRA CD, Jumbo CD, and more. The first step in getting started is to select the account type, which would be a no-penalty CD. If this is not an option then that financial institution does not offer a no-penalty CD account. You will then select what the term length will be. It is in this section that you are able to see what APY is being offered for each term length. .

- Personal Information – After selecting the account, you will fill out the personal information section: first name, middle initial, last name, email address, and phone number. Furthermore, you will have to provide your primary address, city, state, and zip code. After providing your address, you will have to also provide your date of birth, social security number, and employment status. Finally, you will be able to decide if you would like to add a joint account owner at this time.

- Submitting Application – After providing your personal information, you will be able to submit your application. Once submitted, you may have to provide more information to the financial institution by calling their customer service number.

- Providing Bank Information – Once your application is approved, you will be able to provide your bank account information in order to invest your money.

FAQs

Can I Add Funds To Existing No Penalty CD?

The answer to this question is ultimately determined by the timing of when you would like to add money to your account. If it is after the ten calendar day grace period, then no, you may not add any more funds to your no penalty CD.

However, if your term had ended, before the contract automatically renews there is a grace period that allows you to either withdraw a partial amount or all of the money from the account. It is at this point in time that you are able to add more funds to the account in order to earn more money.

Does No Penalty CD Have Lower Rates Compared To Traditional CDs?

Since no penalty CDs allow individuals to pull their money out at any point of the contract, they do typically come with lower interest rates. The interest rates do vary based on the contract term length and what bank you are going through.