Tip #3 – Get Into It As Early As Possible

Sometimes, when you see the value of certain stocks reach unimaginable heights, you wish that you’ve bought even one share so you can participate in the elation of winning. Or maybe you have friends who tried their luck with Bitcoin and enjoyed a crazy windfall after a few months. The temptation can become more intense the more that you hear about these instant millionaire stories.

There’s no denying that. But you should remember that before these people got their rewards, they took risks. And when you’re a newbie, it’s not a good idea to go all in. Hindsight is totally different from foresight although many people mix them up. Do you find ETFs and index funds boring? They could be – but experience tells us that they are likely to outperform the market.

If you’re debating with yourself daily whether to buy or sell with a small amount of money, you won’t get anywhere.

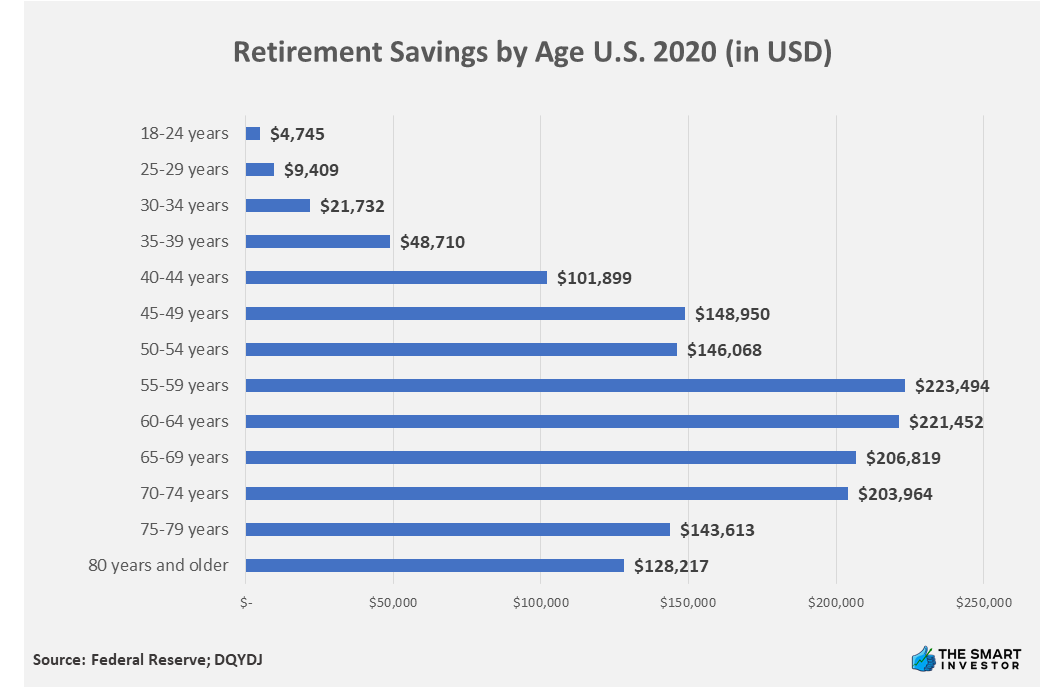

Based on this chart from DQYDJ, retirement savings in the United States increase with age, starting from when young adults join the workforce. Young adults in age 18 to 24 have the lowest savings at $4,745, and the savings increase with age until the 55 to 59 age bracket when the savings peak at $223, 494. Between age 50 and 60, there is a spike in the amount of retirement savings by $77, 426 as retirement savers make catch-up contributions as they approach retirement.

As we’ve said, looking at the boring stocks is like watching the grass grow. They normally move in just one direction but very slowly. However, the exponential power of compounding interest is what will blow you away. Look at the following illustration. If you have $5,000 now and invest it in an index fund that grows six percent per annum, you’ll end up with $50,000 in 40 years.

Chalk up another argument for the adage that says time is money. In investing, every year that you lose in the market can substantially lessen your return in the future. This is why those who invest early have no trouble retiring early. Those who invest later may have to work longer before they can comfortably transition to retirement.

Tip #4 -Don’t Panic When You Lose

Investors who lose sleep over the recent drop in stock prices should realign their portfolios by reducing the ratio of stocks. If you see signs that it’s turning into a bear market (when the price decline is reaching 20% or more), you better act fast if your risk tolerance is low.

You’ll be better off if you lower your stock allocation immediately. You can protect your investment big time by simply adjusting your stock-to-bond ratio by 10% to 20% rather than buying or selling everything of any asset class. If you don’t invest a portion of your portfolio in stocks or any similar growth instrument, you would have to save more money or work longer to get enough retirement stash.

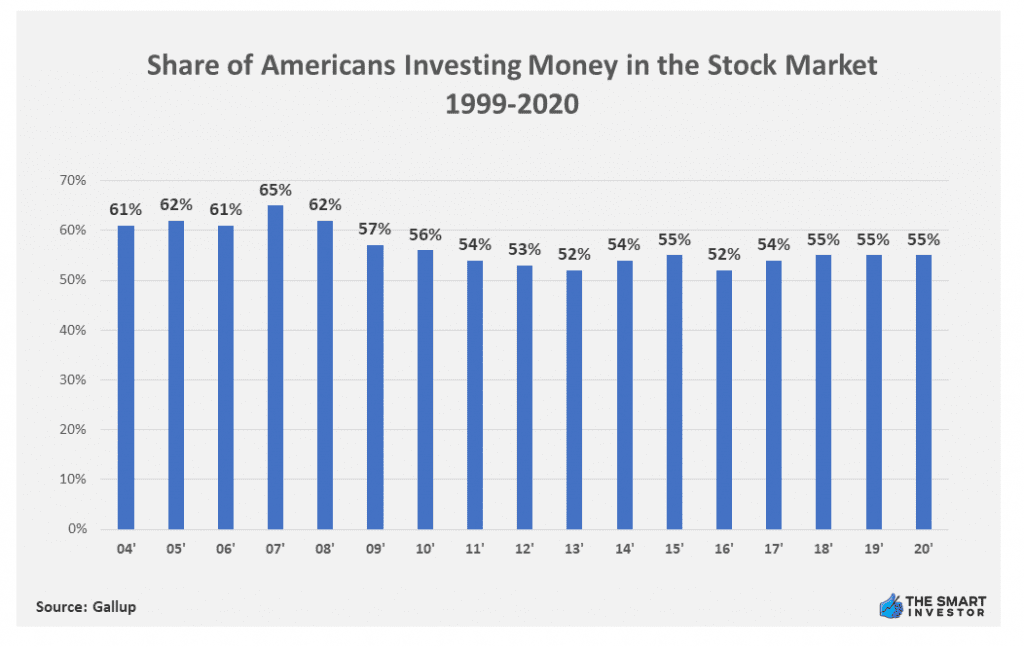

The percentage of Americans investing in stocks has remained steady since 1999, according to a report by

Drastic moves to your investment portfolio – like liquidating everything immediately – may appear to be a safe decision for the moment. But deciding at the height of emotions is never good for you when it comes to investing (or in any other area of life for that matter).

You must have a long-term investment plan that you can follow through the inescapable rollercoaster move of the market. If you follow your emotions, you’ll probably end up buying stocks near market peaks and selling them as they reach the market bottom.

Tip #8 – Learn How To Control Your Emotions

Some investors fail because of their inability to make logical decisions because they get carried away by their emotions. You could probably say that the current prices of assets if a reflection of the collective emotions of the investment community participants. When the majority of investors worry about an asset, they tend to bring down its price. When the majority feel positive about the company’s future, the price usually goes up.

So, it’s normal for investors to feel some anxiety and insecurity when asset prices do not move according to their expectations. If that happened to you, you would probably be asking yourself these questions: Should I sell my position and minimize my losses? Should I hold on to it and hope that the price will rebound? Will it be okay if I buy more?

But observe that even when things are going as you hope them to, you still ask some questions: Should I take this opportunity now before the price goes down? Should I stay because the prices will still go higher? These thoughts may flood your mind especially if you are always watching the price of a security.

Eventually, you will reach a point where the urge becomes so strong that it will force you to take action. And since your decision depended primarily on how you feel, the probability of making a mistake is very high.

Remember that when you buy a certain asset, you should already settle the question of why you are buying that particular asset and not another.

Therefore, you should have an expectation of what the price will do (if your reason is valid). At the same time, you should already make up your mind when to liquidate your holdings, especially if your reason proves to be false or if the asset does not react as you have projected. In short, have an exit strategy ready beforehand. Then, when the time comes, execute that strategy no matter how you feel.

Tip #9 – Consider Automating Your Investments

Dividing your money into four accounts (containers) may seem like a goofy idea but it’s actually a good approach. It’s also quite easy and there’s even a way to automate everything.

This is how it works. Start with your first container and fill it up. Once you fill up your first container, set up automatic instructions with your bank to transfer money from your checking account directly to your investment accounts. This way, you won’t have to do it yourself regularly – it’s a “set it and forget it” model. You can do this online or through your local bank.

You can find plenty of investing platforms that can automate your investments by seamlessly drawing money out of your bank account.

You simply input the frequency and amount that you want, their system will do the actual process. It works to your advantage to have an automated system take the money for your investments or savings when you get your paycheck. It lessens or removes the opportunity for you to spend it before you’ve set aside money for the future.

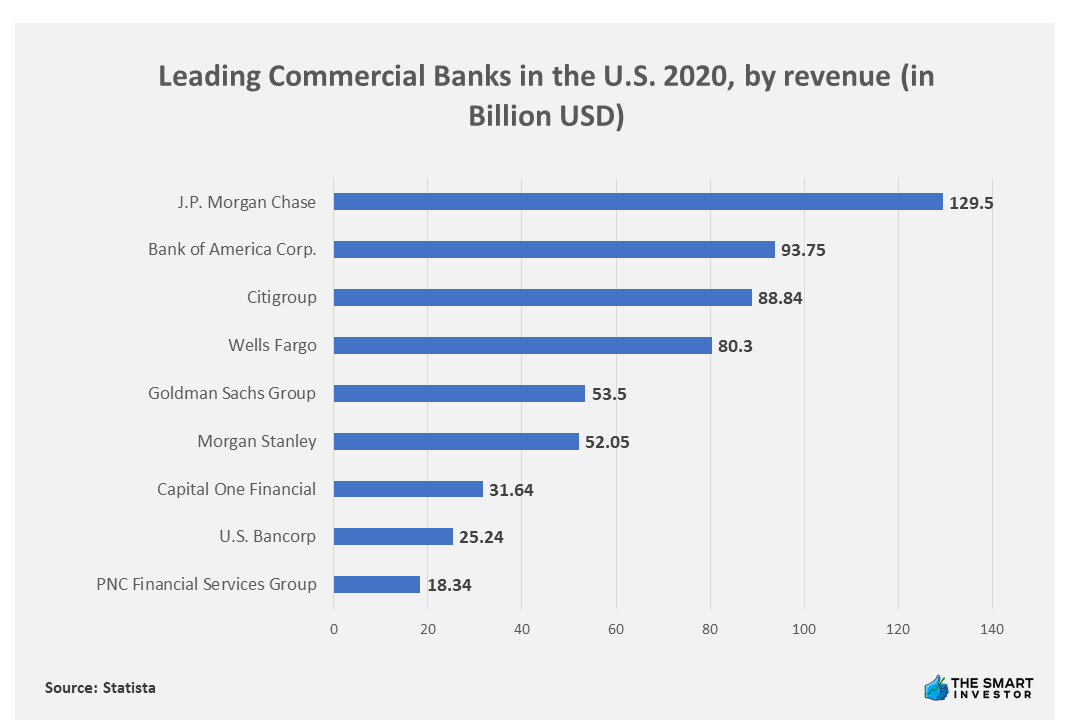

Data compiled by Statista in 2020 of the top 10 largest banks in the United States by revenue ranked JPMorgan Chase in the first position with $129.5 billion. Bank of America Corp took the second position with $93.75 billion, a notable 38.13% short of JPMorgan’s. From the bottom-up, PNC Finance Service Group took 10th place with $18.34 billion in revenue.

Tip #10 – Keep Investing in Yourself

You’ve read all the way here, so it shows you’re off to a good start. Remember that there’s plenty of information out there and this (relevant) information is valuable. Never say that you’re too old to learn something new.

You might need to filter the sources for your investing news and financial markets. Choose the ones from credible sources or those that are not afraid to recommend what’s the best for you. You have access to the Internet at any time and all the time. A single click could open millions of investment guides and tools for your benefit.

Keep in mind that investing in yourself will also reap dividends. But it may cover many different areas. Maybe it’s your knowledge of the stock market that’s developing. Or perhaps you’re learning from the experiences of other great investors who have walked the beaten path. You might also be investing in yourself by becoming more mature and level-headed in your decision-making. The big idea is to keep yourself growing by learning things.

Tip #11 – Don’t Skip on an Extensive Research

It’s surprising how many investors just go ahead and part with their hard-earned money without even spending sufficient time to probe the investment opportunities. They do a short cut by just relying on what “the experts say”, sometimes not even checking who these ‘experts’ are. It may work at first for a couple of times. But if you really want to make sure you’re making good choices, you have to do some groundwork.

The saying “Knowledge is power” is true even in the arena of investing. However, the financial market has its own set of confusing jargons, terminologies, abbreviations, acrostics, and initials that tends to confuse and flood the greenhorn. Try investing in a few financial literacy books that can give you more details about the principles involved in investing or on the stock markets. There are plenty of best-selling business books that can give you a crash course in investing that you may not have received before.

The other benefit is that good research into an investment gives you more confidence in your investment and lessens the anxiety that normally comes with any investment. Be sure you have a full grasp of what you’re venturing into with your money. If you don’t understand something, don’t buy it.

Ask questions, compare brokers and benefits, then ask more questions until you’re satisfied that you know everything you need to know about it. Never purchase an investment because the advertising materials look convincing or the salesperson recommended it to you.